.

not featured

2023-07-21

Borrowing + Credit

published

3 MIN

Credit Scores

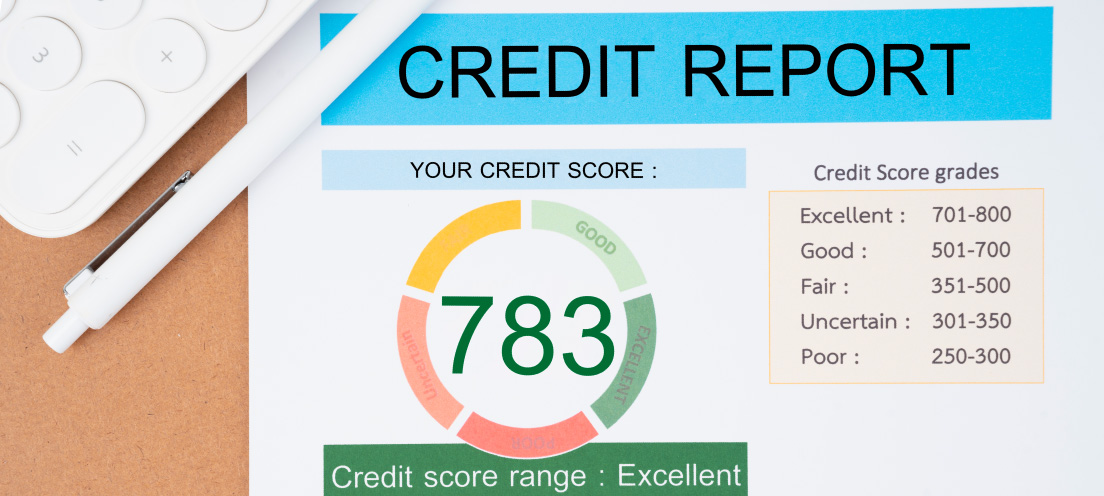

A credit score is a number that potential lenders will use to determine whether they should lend you money, how much, and at what interest rate.

Your credit score is an actual number, between 300 and 850. The higher the number, the better: a score of 740 to 799 is considered very good, though the average is closer to 700. There are companies responsible for tabulating your credit score and providing the score to potential lenders.

Each of the three main credit agencies – Experian, Equifax, and TransUnion - have a score for you based on your credit report at that individual agency. Each agency has more than 200 million files on people who have a credit history because they have used credit, and 4.5 billion are updated in those files every month. The agencies tend to have different information on the people they track, which means your credit report and score will vary from agency to agency.

Those scores are what potential creditors, landlords, employers and insurers look at for an instant judgment on your creditworthiness.

That’s important because lenders believe that people who are creditworthy will pay back what they owe. That’s why better credit reports and higher credit scores make it easier, and cheaper, to borrow. It also makes it easier to rent an apartment, buy a house, get insurance, and a number of other day-to-day essentials.

Avoiding a Bad Score

There are two ways to have a bad credit score. The first, not surprisingly, is by not using credit wisely. That means spending more than you can afford, not paying your bills on time, and having too much outstanding credit, often spread across multiple credit card accounts.

The second is not as intuitive but is still a factor: you can have a bad credit score if you don’t use credit at all. In order to determine your score, there needs to be some kind of history to base it on. So simply cutting up your credit cards, or never having a credit card account, isn’t the path to a high credit score.

One important thing to know about credit scores is that the information is limited to how you use credit – there is no information about your race, religion, medical history, or lifestyle. There’s not even any data on your checking and savings accounts or your investment accounts. It’s all about how you use credit.

Disclaimer

While we hope you find this content useful, it is only intended to serve as a starting point. Your next step is to speak with a qualified, licensed professional who can provide advice tailored to your individual circumstances. Nothing in this article, nor in any associated resources, should be construed as financial or legal advice. Furthermore, while we have made good faith efforts to ensure that the information presented was correct as of the date the content was prepared, we are unable to guarantee that it remains accurate today.

Neither Banzai nor its sponsoring partners make any warranties or representations as to the accuracy, applicability, completeness, or suitability for any particular purpose of the information contained herein. Banzai and its sponsoring partners expressly disclaim any liability arising from the use or misuse of these materials and, by visiting this site, you agree to release Banzai and its sponsoring partners from any such liability. Do not rely upon the information provided in this content when making decisions regarding financial or legal matters without first consulting with a qualified, licensed professional.

Neither Banzai nor its sponsoring partners make any warranties or representations as to the accuracy, applicability, completeness, or suitability for any particular purpose of the information contained herein. Banzai and its sponsoring partners expressly disclaim any liability arising from the use or misuse of these materials and, by visiting this site, you agree to release Banzai and its sponsoring partners from any such liability. Do not rely upon the information provided in this content when making decisions regarding financial or legal matters without first consulting with a qualified, licensed professional.